Rental Property 101

A SUCCESSFUL RENTAL PROPERTY INVESTMENT

Nicolas Deboeuf, CFP®

Financial Planner

Worth Advisors

If you are looking to achieve financial freedom, there’s a good chance that you have considered buying an investment property. After all, owning an income-producing asset that appreciates over time seems like a good vehicle to build wealth and a fun way to learn valuable skills.

While this is true, it is far too common to hear people say that things did not go as planned. In this article I provide a short overview of things to keep in mind when considering getting into real estate.

An investment property is not for everyone.

You will need time and a solid financial foundation to get started. Whether it is looking for contractors, tracking expenses, filing taxes, dealing with tenants or unexpected repairs, your investment property will keep you busy too often at a time that is not convenient. Hiring a property management company can save you some time but will come at a cost.

In addition to finding time, you will also need a strong financial foundation. Replacing a central air conditioner, fixing a leaking roof, could cost you thousands of dollars. Not being able to make mortgage payments because your tenant does not pay the rent could have dire consequences. We recommend having at least 12 months’ worth of living expenses in liquid assets, after making the down payment.

You will also want to have a good credit score (720+) to secure a low interest loan. A $300,000, 30-year term loan with a 4% interest rate will cost you $215,607 in interest over the term of the loan. In comparison, that same loan with a 6% interest rate will cost you $347,515 in interest, 61% more (1).

Looking for your first property.

Just like any investment, there are good and bad apples. We recommend focusing on finding a place that meets the following criteria:

- Located in a currently growing area

- Low maintenance

- Good overall condition

- Attractive household amenities

- Low gross rent multiplier relative to other properties (see below)

A large backyard, a high-end kitchen or a pool can be attractive, but remember that you are not looking for your dream home. The end goal is to make a profit, stick to the numbers and do not let your emotions cloud your real estate judgment.

The cash flow vs. capital appreciation dilemma.

Understanding how your investment will make you money is key.

The main way a rental property can make money is through cash flow. It is the difference between the rent collected and all operating expenses. That form of income is very important because it is liquid, meaning it is readily available, can be reinvested or used to cover upcoming expenses.

Another way to make money is through capital appreciation, a rise in your investment’s market price. While home prices have skyrocketed in recent years, they have historically appreciated at a rate of 5.3% per year over the past 20 years (2)

First-time investors and investors with a relatively low cash reserve should stick with properties that offer positive cash flow at the end of the month, rather than speculate on high projected appreciation properties.

Crunching the numbers

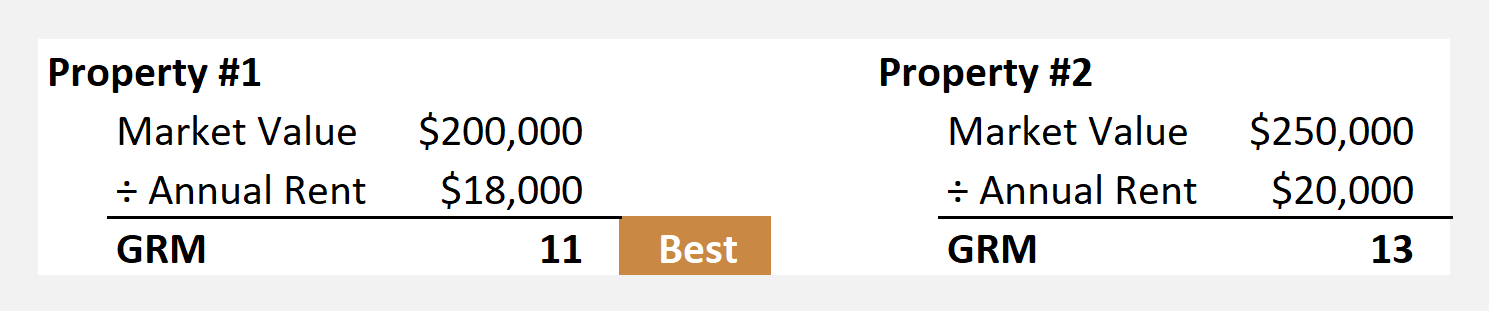

The Gross Rate Multiplier (GRM) functions as the ratio of the property’s market value over its annual gross rental income. While you should not rely solely on that ratio, it is a quick and simple way to compare and screen properties. A lower value is best.

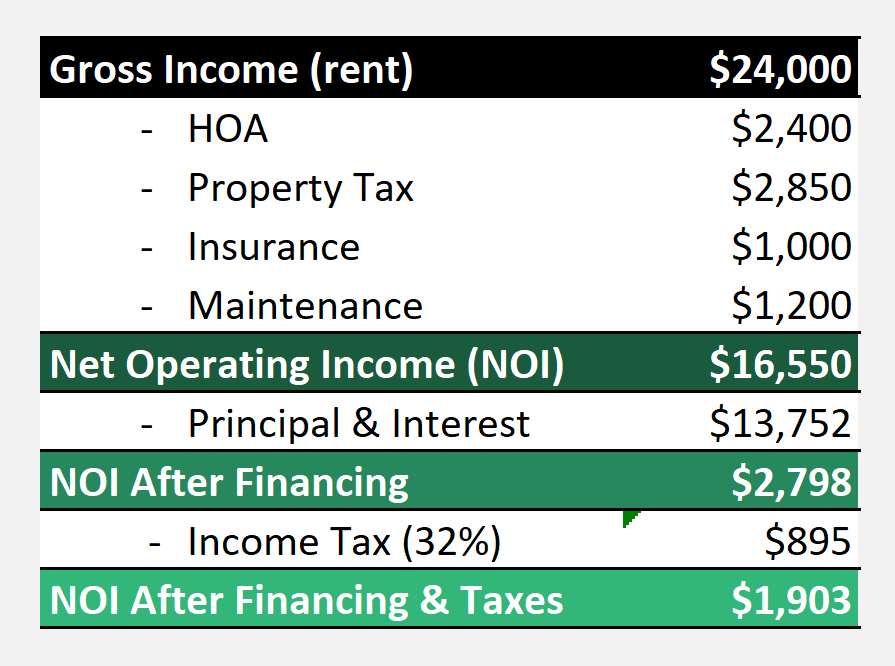

The Net Operating Income (NOI) is a calculation used to analyze the profitability of income-generating investment. The formula is straightforward, subtract all operating expenses from gross operating income.

Do not forget about taxes.

You are responsible for reporting rental income to the IRS, even if it is paid in cash. A tax specialist can help you reduce your income tax liability by taking the appropriate deductions, such as interest, property taxes, depreciation, travel expenses, advertising, utilities for instance, etc. Tracking your expenses will be key.

You will also be responsible to report capital gains at the disposition of the property. Failing to do so could lead to large tax penalties from the IRS. Once again, your tax specialist will be able to give you options to minimize or defer capital gains tax. A 1031 exchange for instance, will let you swap your investment property for another “like-kind” property without recognizing a gain.

Playing the Long Game.

Finally, you will have to play the long game. Sellers must pay their own closing costs and those costs can add up to 8% –10% (3) of your home’s final sales price. You will incur closing costs at the time you decide to sell the property. If your home sells for $300,000, then, you can expect to pay from $24,000 – $30,000 in closing costs.

We highly recommend discussing this with your advisor prior to making any financial decisions.

References

1 – https://www.zillow.com/mortgage-calculator/

2 – https://www.ceicdata.com/en/indicator/united-states/house-prices-growth

3 – https://www.rocketmortgage.com/learn/closing-costs-for-seller